Maintaining Momentum

As 2019 winds down, enthusiasm and optimism around private brands seems sky-high, and the outlook toward the future seems just as lofty.

“We do believe at Ahold Delhaize USA that this is a virtuous cycle,” says Juan De Paoli, senior vice president of private brands for Salisbury, N.C.-based Retail Business Services, an Ahold Delhaize USA company. “The momentum will continue to grow, and I believe that we are going to see exponential growth in private brands over the next five to 10 years.”

Retail Business Services provides services including the development of private brands for Ahold Delhaize’s grocery chains such as Stop & Shop, Giant Food, Giant/Martin’s, Food Lion, Hannaford and the online grocer Peapod. De Paoli says the company’s private brands are “thriving” because they drive consumer loyalty, shopping trips, and help Ahold Delhaize USA’s chains innovate and differentiate. “Not to mention that millennials and Gen Zers are a lot more open to or are more private brand-driven because of that perfect intersection of quality and value,” he adds.

Having witnessed more than 30 years of experience in private brands at companies such as Topco Associates LLC, Jewel Food Stores and Shaw’s Supermarkets, Jim Wisner believes the current state of private brands is succeeding because there’s a decline in market power among the large, multinational consumer goods companies, and that private brands have stepped up by offering more than just a lower price like cleaner labels and premium products.

“We genuinely are in a golden age for store brands,” says Wisner, the president of Wisner Marketing in Lake Forest, Ill. “And it is one that, quite honestly, there are very few headwinds and a lot of tailwinds.”

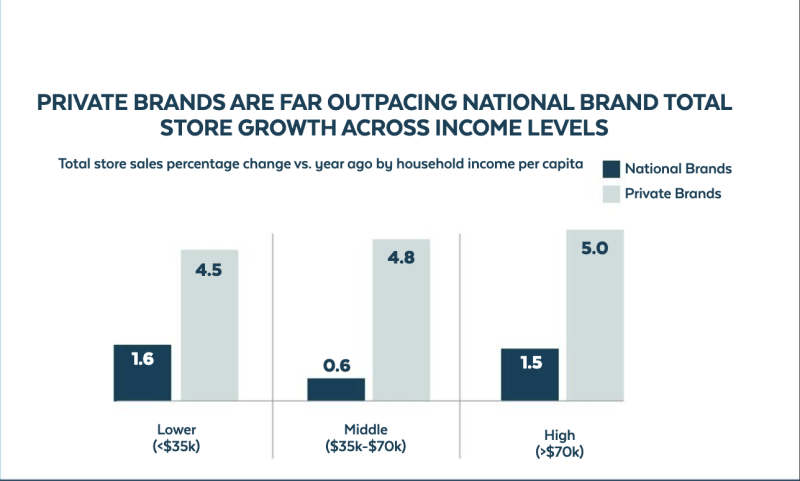

Recent numbers support this: Across lower-, middle- and higher-income levels, store brands are outpacing national brands, seeing roughly 5% growth at each income level in total store sales versus a year ago, compared to national brands seeing just over 1%, according to a November report from the Food Marketing Institute (FMI) and IRI. In that same report, annual gains from private brands far exceeded those of manufacturer counterparts across store departments, too. Refrigerated foods saw a 6.5% bump versus a mere .3% bump by national brands; general merchandise increased by nearly 8% while national brands dropped a third of a point.

IRI, in a “Consumer Connect Survey” released last month (see more on page 5), found that nearly 60% of consumers felt their households were in good financial shape, dispelling any economic downturns driving sales of private brands. In fact, 65% of households making at least $35,000 annually felt groceries were easily affordable. Not surprisingly, the percentage grew as the income levels per household grew.

The IRI study found consumer attitudes shifting toward private label, noting that two-thirds of consumers felt store brand products were as good if not better than the national versions, and that private label has an impact on why a shopper chooses a store to shop. More than half of the Gen Z and millennial shoppers said they picked stores to shop based on their private label offerings, according to the study.

“For the longest time, private brands were always price driven — price, price, price — so as long as you were following the brands fast, you were successful,” says Doug Baker, vice president of industry relations at FMI. “They’re no longer a private label. They are now a private brand. Consumers see them the same way they see PepsiCo, Frito-Lay, Kellogg’s, and they hold them to the same standards.”

Wisner feels in some cases — like The Kroger Co.’s Simple Truth brand (delivering on a natural and organic promise) — that store brands might even be doing better than national brands at giving consumers what they want. “Somebody once characterized it as we’ve seen a switch from value to values, which I think sums it up very well,” he notes.

In the IRI report, of all the consumer households surveyed, nearly 100% said they buy private brands today. Store brands are clearly established and seeing success. The question becomes: With private brands footed on higher ground and feeling a blustery tailwind behind them, how do they maintain the momentum?

Keys to momentum

Baker says a major play for private brands going forward is to become more innovative, saying there’s no rule that a private brand must wait for a national brand to launch first. FMI is actually partnering with IRI this year to do some work on helping private brands take more risks like national brands and educate them on how to “test, learn and pivot,” a concept that national brands follow when launching new products.

Baker says Target’s new Good & Gather line is an example of a store brand that put in the work to test the brand, learn and make changes before launching, and he expects to see more retailers do the same. He also adds that retailers need to continue to appeal to the younger consumers to maintain momentum.

“Understand the millennials and Gen Zers,” he says. “If you want to be relevant 10 years from now, look at that consumer base that’s going to be the financial power 10 years from now.”

Baker notes that Gen Z shoppers love to shop in brick-and-mortar stores, as opposed to buying online because their parents buy online, but they want to have their mobile phones and access to technology inside the stores.

De Paoli says producing private brands with cleaner products will grab the younger shoppers and build momentum. Ahold Delhaize USA set a company goal to have 100% clean labels by the year 2025. The retailer’s Nature’s Promise brand delivers against the goal and recently added a Nature’s Promise Kids line of clean products that follow strict nutritional guidelines, and the company just launched Nature’s Promise cleaning products in packages that are made from 100% post-consumer recycled content.

“Last but not least, efficiency is essential,” De Paoli says. “Private brands will always continue to compete on price.”

Wisner believes companies need to continue to provide premium private brand products, saying the premium category has gained its share of private brands by three points in the last year.

“If you look at premium, unique and different, I mean the innovation is finally — much like it does in Europe — starting to come more from the private brand side and less from the branded side,” Wisner says. “And that’s a sea change.”

Trader Joe’s hangs its nautical hat on its ability to deliver premium products and has grown a rabid fan base around its products. The company has several online influencers dedicated to the retailer with hundreds of thousands of followers each.

Baker says creating loyal shoppers like Trader Joe’s is imperative for private brand future success. “If you create a loyal shopper, the margin and the profit are there,” he adds.

Where to improve, what to avoid

While he may agree with the importance of loyalty, Bob Anderson, president and CEO of Fayetteville, Ark.-based Store Brand Consulting, has strong warnings for how retailers and private brand manufacturers approach premium or innovative products. Anderson is a veteran of the store brands industry, credited with beginning Walmart’s Great Value brand and leaving it at a time it was worth $17 billion.

Anderson says chasing trends or odd flavors just to do it could set private brands back long term, spurning more shoppers than gaining them. If a new idea like pickle-flavored ice cream fails, the store brand loses some integrity and even worse so does the store. Anderson’s biggest concern is that too much SKU proliferation and innovation aren’t in the interest of protecting the brand.

For example, when Anderson was at Walmart, where he was vice president and general manager of private brands from 1990 to 2007, the retailer rolled out Sam’s Choice chocolate chip cookies that were made with butter and had 39% more chocolate chips in them. He says those were things that made the cookies premium compared to the national brand equivalent.

Premium needs to be defined, not just throwing some exotic flavors onto a pizza and calling it premium, and boxing it under a new store brand name. “It makes it unusual, but it doesn’t make it premium,” Anderson adds.

He stresses that private brands don’t need to be the first ones in on a new item or category. National brands have the resources and R&D money to experiment, and private brands can come in after with a twist on an item and make it better.

“You need to understand the awesome responsibility that it is to manage a brand — how many SKUs; how many dollars you do; how many lives you effect from a customer base, company base and the suppliers doing business with you,” Anderson says. “You need to understand that if you don’t leave customers with a good taste in their mouths, they won’t come back again.”

Similarly, Anderson warns about over-SKUing a store with too many private brands. “You don’t have enough people to watch over the quality, the integrity, the manufacturing and the supply chain for all of them.”

Rather than spending time on creating so many SKUs, Anderson would rather see private brand teams working directly with suppliers, building better relationships with them and helping those suppliers create more efficient operations that are ready for the future.

He wonders further if SKU proliferation is the reason sales are up for private brands in the industry. “Is it because you walk into Walmart, and they have 12 doors of private label pizza now?” he asks. “Is that where it is? Sales are up but, most importantly, are profits up?”

Another watchout for private brands, according to Baker, is packaging. The recent “Power of Private Brands” report from FMI found that nearly 20% of consumers said store brand packaging makes the products look as if they’re of lesser quality than the national brand.

The digital future

One area where national brands are threatening to curb private brand momentum is in building out more powerful online strategies. Ali Dibadj, a partner with Alliance Bernstein in New York, recently spoke at the Private Label Manufacturers Association’s Private Label Trade Show and said brands are fighting back by outspending retailers on promoting products online, assuring national products make the top of the search list and are on that first page on Amazon. (See a recap of the Dibadj session and Private Label Trade Show on page 26.)

Wisner agrees with Dibadj. “Most of the national brands have moved much faster in understanding the online and e-commerce world,” he says. “They are far more sophisticated in terms of digital marketing.” Wisner likens the task in front of private brands as going from a retailer’s in-store, 70,000 square feet of shelf space down to 70 square centimeters of online screen space where only three items get listed.

Wisner’s company recently performed a full-day workshop with the Italian Trade Agency on how to leverage digital communications to get content and messaging out about the authentic nature of the Italian private products the agency does for its retailer partners.

It’s in the digital marketing space where Wisner sees retailers needing to improve, although he’s encouraged by retailers like Kroger, H-E-B, Hy-Vee and The Albertsons Cos., which have opened tech and culinary innovation centers. “Those are going to drive a lot of growth in a good way,” Wisner says.

De Paoli agrees that national brands are pushing private brands in the digital space, and it’s important for private brands not to get complacent. “Private brands need to keep up with the industry and in some cases set the pace.”

Digital work for private brands includes getting more involved in blockchain strategies, integrating private brands into the retailer’s data platforms, building out programs to fuel online shopping and producing digital information on products from scanning labels. Retail Business Services, for example, is the biggest participant in SmartLabel, a worldwide program giving consumers access to detailed information on 11,000 private brand products.

In September, supporting FMI’s Family Meals Month program, various retailers used social tools (in addition to other tactics) to promote the importance of families sitting down together for at least one meal a week. Retailers like Kroger used Twitter to showcase private brand products that could be used to make a meal for just $10. Other participants included Weis Markets, ShopRite and more.

The FMI report with IRI also looked at the biggest threats facing private brands and 70% of respondents said “a lack of innovation,” with more than 40% citing a lack of data and insights, and home delivery online sales as threats.

Baker agrees that it’s important for retailers to get better in the digital space as they look to build momentum, but he does say, looking forward, that the U.S. private brand industry will never achieve European penetration levels of 40 to 50%. He acknowledges some retailer brands may achieve success close to it, but he says it’s an unrealistic benchmark.

He stresses that retailers simply need to focus on loyalty. “I think, ultimately, as long as we don’t stop listening to consumers, and we don’t stop putting margin in front of loyalty, then private brands are going to continue to play an important role for the retailer,” he says.