Shelf-Stable Foods Report: From Soup to Nuts

In the middle of the store, it was the year of the experimental grocery shopper. Throughout 2020, shoppers took fewer trips to minimize their exposure to COVID-19 and make larger stock-up purchases as dining-out options shrank during the pandemic and cooking at home became the norm. Limited quantities of produce and fresh meat in many parts of the country forced cash-strapped consumers to adjust their routines and look for items that were more widely available, stretched their budgets further and lasted longer.

As a result, a large swath of shelf-stable products at the center store — many in traditional packaged goods categories that have been falling out of favor for years — suddenly got a second look. “People like to buy fresh ingredients, but when those things are taken away — whether it’s because they lost their job, it’s not on-shelf or they only want to shop every other week — they will of course try new things,” said Andrew Russick, vice president of sales and marketing at Pacific Coast Producers, one of the largest suppliers of private label canned tomatoes and other fruits.

Those “new” things included an array of familiar kitchen staples: everything from cereal and oatmeal to nuts, beans, canned vegetables, rice, dry pasta and soup. Russick says that retailers’ pent-up demand for canned tomatoes following an initial run on shelves in March sent the company’s sales up anywhere from 8-12% in late summer and early fall, depending on the product and region. “Shoppers discovered that moving from fresh to shelf stable didn’t hurt them at all,” he said. “They got something that’s portion controlled, all prepped and ready to cook. And the quality was just as good or better than what they were getting from a national brand.”

Similar trends played out in canned peaches and other fruit categories, said Russick. “There is a slight bias around shelf-stable because people think, ‘Well you wrap a can around it and it’s not as fresh’,” he said. “We’ve always known that canning is the freshest thing out there. It’s picked in the field and five hours later it’s in the can. It brought people into purchasing things they wouldn’t normally consider."

Varying Strength of Private Label

By now, it is widely accepted that 2020 was a banner year for store brands. Indeed, the pandemic accelerated the shift toward smaller manufacturers and private brands, as national food manufacturers struggled to keep products on shelves. Big food companies lost 1.3 share points, or $12 billion in sales, to small CPGs and private brands, according to an IRI report published in January 2021.

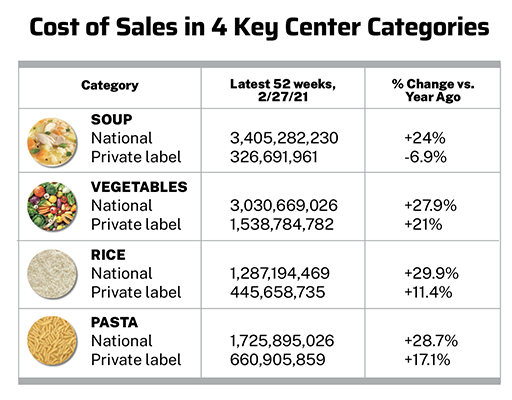

Yet the relative strength of private label was not spread equally across all categories. In some center-store categories with the biggest volume increases, the share of private label actually decreased compared to national brands. Soup, dry pasta and rice, for example, all saw overall jumps of more than 20% for the 52 weeks ending Feb. 27, according to Nielsen data (see chart). The share of private label in each of these categories dropped anywhere from 2-3% during the period.

In soup, it appears that a rising tide lifted all boats. Pantry loading in the early spring provided a boost to national brands like Campbell’s and Progresso, as consumers stuck with the brands they grew up with, said Dan Carley, vice president of sales and marketing for store brands at Baxters North America. “After that initial surge, brands stayed up 15%-20%, took a dip in September and came back up again,” he said. “Brands drove quite a bit of the strength in the category but private label also did well. Brands were up about 30%-35% at the end of the year and private label was up about 15%-20%.”

This year has been more challenging for the soup category. In its latest earnings announcement last month, Campbell’s warned of waning sales as consumers began to dine out more and get back to the office. Carley at Baxters expects the category to be down anywhere from 5%-10% by year’s end, but said the company hopes to make inroads against branded soups with new flavors and formats like pouches and single-serve toppers, with several new SKUs available starting in July.

The picture is brighter in the $2 billion rice category, which had more upside momentum heading into the pandemic. Total sales were up 3.9% for the 52 weeks ending Feb. 29, 2020, per Nielsen, with slightly higher gains in national brands than private label. “Ready-to-serve rice is a super easy side dish, and the pandemic only drove this trend further,” said Carley. Private label sales increased by triple digits for several weeks last spring, though from a much lower base than national brands, he said. He expects the category to maintain a 20%-30% growth rate this year.

“More consumers are going back to restaurants, so when they are cooking at home, they will be looking for something different [than plain rice],” he said. “We’re doing new globally inspired flavors, including a Chimichurri, a Moroccan curry and a separate lineup with lentils, so you’ve got a plant-based protein with some added flavors.”

Down Time: Nuts, Snacking and Baking

Tales of quarantine cooking and baking blanketed the Internet in 2020, as consumers had more time for leisure activities and could put more thought into their meals and snacking habits. Two categories that benefited from these trends, not surprisingly, were nuts and baking mixes.

Nut sales had been growing steadily prior to last year, thanks in part to the product’s reputation as a healthier snack option, said Krista Daly, director of marketing at Marathon Ventures, a producer of private label nut products including snacking and baking nuts. “During the pandemic, we found each customer had its own story with anywhere between 20%-50% growth, depending on the channel and category, with a trend toward bulk purchases and larger packaging size options,” she said. “There was some disruption in smaller package [and] grab-and-go impulse items. Otherwise, the growth trends were amplified.”

Bryn Garcia, vice president of retail sales and business development at private label almond producer Select Harvest USA, said that the almond segment continues to benefit from the nut’s perception as a low-carb, high-protein snacking source and as an alternative baking option for customers seeking healthier choices.

“We had an extremely strong year for almonds last year,” Garcia said. “We saw the majority of our lift early on at the beginning of the pandemic onset when retailers were struggling to keep enough products on-shelf. Their customers were stocking up in massive quantities in order to prepare for lockdowns for undetermined lengths of time, and retailers were putting in back-to-back purchase orders with us and many other suppliers to keep up with demand.” While almond sales were fairly evenly distributed between private label and national brands, she said, “Private label took a bit of a hit once the lockdowns began to lift in many states and retailers were overbought on their own branded items.”

Private label disruption is a growing story in the baking mixes category, which traditionally has been dominated by national brands Pillsbury, Duncan Hines and Betty Crocker. However, skyrocketing demand during the pandemic has begun to slowly open the door for store brands.

“Major retailers are finally realizing how important their owned brands are, and particularly in the premium and clean label area,” said Fern Phillips, CEO of Little Big Farm Foods, which produces more than 60 baking mix SKUs for brick-and-mortar and online specialty retailers, as well as a line of branded mixes with the company’s name. “So far this year, private brand growth in the premium segment is really picking up. There is more opportunity to do development for retailers and specialty brands.”

Despite operating in an indulgence category (Little Big Farm Foods’ apple cider donut mix is among its top sellers), private label baking mixes can differentiate from national brands by meeting the needs of shoppers’ various dietary restrictions, said Phillips. “I think gluten-free will always be around, but programs like keto are really catching on,” she said. “You can use almond flower or some other kind of unbleached and un-enriched flour [for a healthier mix]. It’s a processing difference. The national brands are trying to keep up by looking more organic and natural, and they are keeping prices down by decreasing net weight."

Post-Pandemic Trends

Many of the above trends began to take shape well before 2020 and, according to the suppliers, should continue to strengthen once the pandemic wanes. “We anticipate continued strong demand, less the pantry filling spikes, with the slow and steady return of food service,” Garcia said. “While in-home cooking and baking has certainly increased, those activities will be affected by the reopening of restaurants. However, we believe growth will remain above pre-pandemic levels. Snacking, on the other hand, will continue on a high growth trajectory regardless as people have moved beyond the traditional three-meal plan to snacking all day.”

Daly agrees. “The continued importance of better-for-you snacking options and overall health benefits of the food we put into our bodies will drive growth in the healthy, natural, minimally processed space,” she said. “I’m thrilled to see people paying greater attention to the way food and it’s nutrients effect our body and how we feel, and I hope that is a trend that lives on.”

Independent private label experts believe that the push toward clean label products will also accelerate this year. Jim Wisner, president of Wisner Marketing Group, said that interest in sustainability actually increased during the pandemic, perhaps counter-intuitively. “You’d think that with people just trying to get their hands on products and reverting back to brands they knew as a kid, something that could be considered trendy like clean label would take a back seat. In fact, the opposite happened,” he said. “One explanation is that there was so much concern about health in general, it got people more engaged in topics like the environment.”

Of course, none of this bodes particularly well for manufacturers of processed foods. Still, the long-term outlook for the center store may depend on whether many of these iconic brands can keep up with consumer demand for new flavors and lighter versions of their original products. “We expect conditions [in the center store] to eventually drift back to what they were before,” Wisner said. “The pandemic disrupted some of the sales trends but it didn’t change the overall pattern.”